On Tuesday, U.S. stocks surged with the Dow Jones Industrial Average gaining 0.40%, the S&P 500 rising 0.52%, and the Nasdaq Composite adding 0.58%. This upward trend was fueled by a significant drop in Treasury yields, down 13 basis points to 4.65%, as investors sought safer assets due to the Israel-Hamas conflict. Positive market sentiment and anticipation of economic data releases also contributed to the market’s positive performance. The U.S. Dollar faced another decline, influenced by Wall Street’s performance, as key economic data and Federal Reserve minutes awaited scrutiny. In the currency markets, the Euro, British Pound, Australian Dollar, and New Zealand Dollar all saw gains against the U.S. Dollar, while the Japanese Yen experienced a setback.

Stock Market Updates

On Tuesday, U.S. stocks experienced a notable rise, with the Dow Jones Industrial Average surging by 0.40%, or 134.65 points, to close at 33,739.30, while the S&P 500 gained 0.52%, ending at 4,358.24. The Nasdaq Composite, which has a tech-heavy focus, added 0.58%, reaching 13,562.84. This increase in stock prices was partly attributed to a significant decrease in Treasury yields, with the benchmark 10-year Treasury yield falling by nearly 13 basis points to approximately 4.65%. This decline in yields occurred as investors sought safer assets amid the ongoing Israel-Hamas conflict. The bond market had been closed on Monday due to Columbus Day, and this shift in bond yields was the initial market reaction to the geopolitical situation. Additionally, falling oil prices after a previous rally provided further relief to investors. Despite initial concerns over rising interest rates and the conflict’s geopolitical risks, optimism grew in light of a strong September payrolls report and anticipation of upcoming third-quarter earnings releases.

One key contributor to the market’s positive performance was the shift in bond yields. This shift was perceived as a potential indication that the recent rapid increase in yields might be slowing down. Investors also began looking beyond the geopolitical concerns posed by the Israel-Hamas war and focused on economic factors, with anticipation building for inflation data releases scheduled for later in the week. Small-cap stocks, such as those in the Russell 2000 and the S&P Small Cap 600 index, demonstrated strong performance, gaining just over 1% each during the trading session. This marked the Russell’s fifth consecutive day of gains, a feat not seen since July. However, some investors remained cautious, viewing the rally as a reaction to previously priced-in negative sentiment and oversold conditions. Despite the market’s positive day, concerns about the ongoing inflationary pressures persisted, with some experts suggesting that the fourth quarter may be relatively flat despite expectations of positive earnings growth for the third quarter. Notable stock movements included PepsiCo’s 1.9% rise following better-than-expected third-quarter results and an upward revision of its earnings outlook, as well as positive gains for energy and industrial companies like Enphase Energy (5% increase) and Generac Holdings (3.8% gain).

Data by Bloomberg

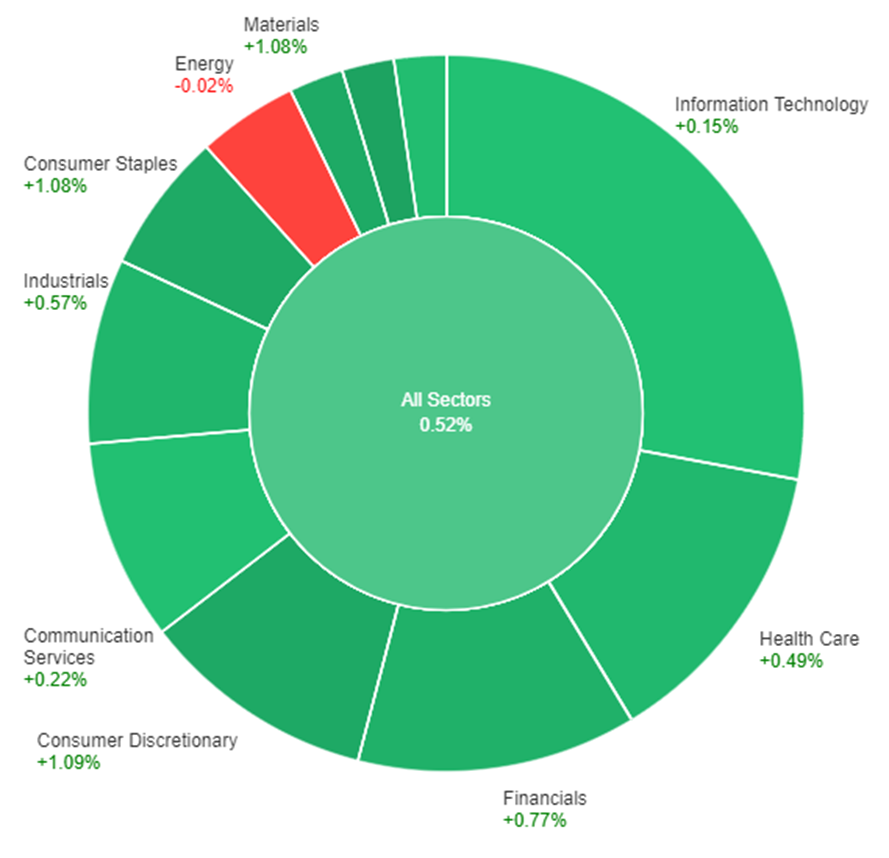

On Tuesday, the stock market experienced overall gains, with all sectors combined rising by 0.52%. The biggest increases were seen in Utilities (+1.36%), Consumer Discretionary (+1.09%), Materials (+1.08%), and Consumer Staples (+1.08%). Other sectors also saw positive movements, but to a lesser extent, with Financials gaining 0.77%, Industrials increasing by 0.57%, Health Care by 0.49%, Real Estate by 0.30%, Communication Services by 0.22%, and Information Technology by 0.15%. Energy was the only sector that showed a decrease, with a decline of -0.02%.

Currency Market Updates

The US Dollar faced another decline as positive market sentiment persisted and US yields remained distant from recent peaks, with the 10-year yield settling at 4.65% and the 2-year yield falling below 5%. This depreciation pushed the DXY index to its lowest daily close since September 18, dipping below 106.00. In the coming days, market watchers are eagerly awaiting key economic data and releases from the Federal Reserve. The US will unveil the September Producer Price Index (PPI), which could carry significant consequences if it surprises to the upside. Furthermore, the Federal Reserve will publish the minutes from the September FOMC meeting, offering insights into the central bank’s economic outlook. Meanwhile, the US Dollar’s decline was influenced by Wall Street’s positive performance, and despite a modest pullback in crude oil prices, commodity markets demonstrated mixed movements.

In the currency markets, the Euro made gains against the US Dollar, surpassing the 20-day Simple Moving Average for the first time since August, reaching a level around 1.0600. Key resistance for the EUR/USD pair is anticipated at 1.0630. The British Pound also benefited from short-term momentum, with GBP/USD rising above the 20-day SMA and hovering near 1.2300. The Japanese Yen experienced a setback, as rising equity prices and a modest rebound in yields pushed USD/JPY above 149.00, though it later retraced to 148.60. In contrast, the Australian Dollar saw gains for the fifth consecutive day, with AUD/USD maintaining a position above 0.6400 and aiming to extend its recovery, with significant resistance awaiting at 0.6500. The New Zealand Dollar followed a similar trajectory, holding above 0.6000 and posting its highest daily close in two months at 0.6040. Finally, USD/CAD remained relatively stable around the 1.3600 range as the Canadian Dollar consolidated recent gains, with a flat 20-day SMA at 1.3555 offering a potential point of interest.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Reaches Two-Week High at 1.0620 Amid US Dollar Correction and Geopolitical Concerns

In recent trading, the EUR/USD pair experienced a surge to 1.0620, marking its highest level in two weeks, before slightly retracing to the 1.0600 range. This upward movement is fueled by an improved market sentiment and the ongoing correction of the US Dollar, compounded by concerns over geopolitical events. The spotlight now turns to the upcoming US inflation data, particularly the Producer Price Index (PPI) and Consumer Price Index (CPI), as well as the release of the FOMC minutes, which will shed light on the Federal Reserve’s monetary policy expectations. Meanwhile, in Europe, the German Consumer Price Index remains stable, but the sluggish inflation and a pessimistic economic outlook suggest that the European Central Bank is likely done with interest rate hikes.

Based on technical analysis, the EUR/USD went up on Tuesday and managed to reach the upper band of the Bollinger Bands. Right now, the EUR/USD is trading below the upper band, which suggests a chance for a small downward move to reach the middle band of the Bollinger Bands. The Relative Strength Index (RSI) is at 59, indicating that the EUR/USD is currently trying to return to a neutral position with a bullish bias.

Resistance: 1.0616, 1.0674

Support: 1.0530, 1.0460

XAU/USD (4 Hours)

XAU/USD Shines as Investors Seek Safety Amid Fed’s Monetary Tightening Hints and Easing Dollar

Spot Gold has extended its weekly rally to $1,865.35 a troy ounce as investors continue to seek safety, while the US Dollar eases following comments from different Federal Reserve (Fed) officials, hinting at no more monetary tightening. Fed Vice Chair Philip Jefferson and Dallas Fed President Lorie Logan noted that higher Treasury yields help tighten financial conditions and could offset the need for additional hikes, while Atlanta Federal Reserve President Raphael Bostic believes the policy rate is sufficiently restrictive to reach the 2% inflation target, despite acknowledging there’s still a long way to go. Meanwhile, tensions in the Middle East have fueled demand for government bonds, resulting in easing yields, making Gold an attractive option for investors.

Based on technical analysis, XAU/USD is consolidating on Tuesday creating a narrow range in the price movement. Currently, the price of gold is moving between the middle and upper bands of the Bollinger Bands. The Relative Strength Index (RSI) currently stands at 65, signaling a bullish bias for the XAU/USD pair.

Resistance: $1,874, $1,887

Support: $1,845, $1,829

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| USD | Core Producer Price Index | 20:30 | 0.2% |

| USD | Producer Price Index | 20:30 | 0.3% |