The Federal Reserve’s indication of maintaining high-interest rates led to a stock market dip, impacting indices like the Dow Jones, S&P 500, and Nasdaq Composite. This stance affected sectors including housing, reflected in the lowest existing home sales since 2010, impacting companies like Lowe’s and American Eagle. Amidst this, Amazon’s stock fell due to Jeff Bezos’ shares sale, while Nvidia faced a slight decline ahead of its earnings announcement. The dollar saw a rebound after a significant drop, influenced by FOMC minutes and market volatility from weak economic data. Currency pairs like EUR/USD faced downward trends, diverging from USD/JPY’s speculative long positions. Expectations on rate cuts varied between the ECB and Fed, impacting movements in pairs like USD/CAD and USD/CNY. Future market sentiments hinge on upcoming economic releases like U.S. durable goods and jobless claims, likely affecting currency valuations and sentiments.

Stock Market Updates

The stock market saw a decline following the release of the Federal Reserve meeting minutes, which indicated no plans for interest rate cuts. This led to the Dow Jones slipping by 0.18%, closing at 35,088.29, while the S&P 500 dipped 0.20% and the Nasdaq Composite fell by 0.59%. The Fed emphasized the need for a “restrictive” policy to combat potentially stubborn or rising inflation, maintaining the benchmark rate at 5.25% to 5.5%. Market expectations suggest the Fed will maintain this stance through its December meeting, with potential rate cuts anticipated from May onwards.

This environment of sustained higher rates impacted various sectors. Housing data revealed a tough month for homebuyers, with existing home sales dropping to 3.79 million units, the slowest pace since August 2010. Companies like Lowe’s and American Eagle faced stock declines due to reduced sales outlooks and weaker operating income guidance, respectively. Additionally, Amazon’s shares dropped 1.5% following news of former CEO Jeff Bezos selling 1.67 million shares. Amidst this, Nvidia, despite hitting an all-time high on Monday, experienced a slight dip in shares by 0.9% on Tuesday ahead of its earnings announcement.

Data by Bloomberg

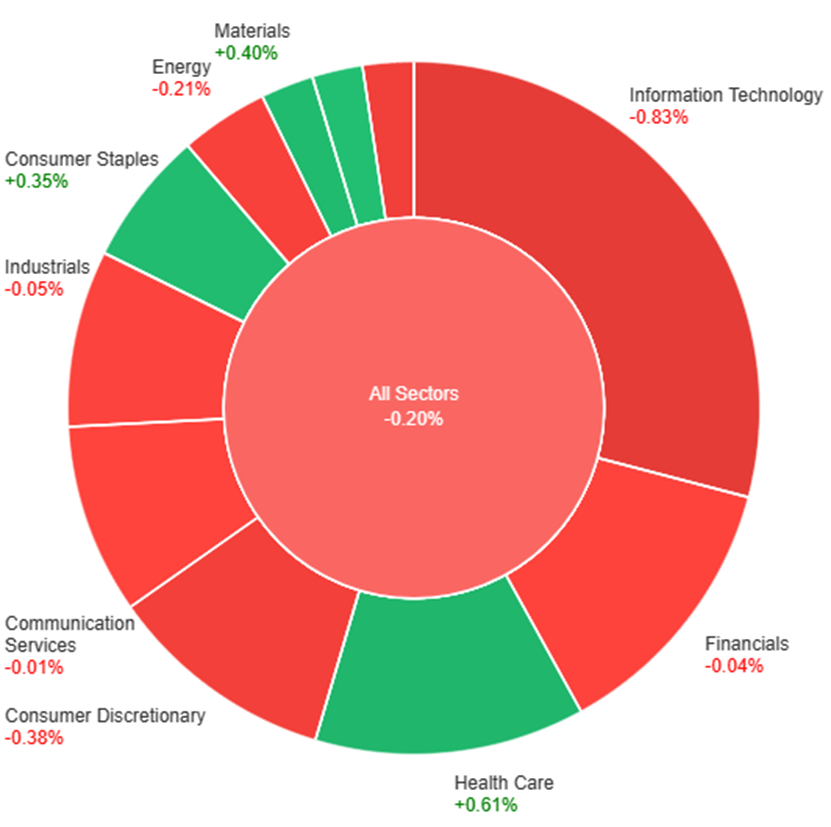

On Tuesday, across all sectors, there was a slight downturn of 0.20%. However, some sectors experienced positive growth, with Health Care leading the way at +0.61%, followed by Materials (+0.40%), Consumer Staples (+0.35%), and Utilities (+0.22%). Conversely, Information Technology witnessed the most significant decline at -0.83%, while Consumer Discretionary (-0.38%) and Real Estate (-0.47%) also faced notable decreases. Communication Services showed marginal negative movement at -0.01%, and Energy (-0.21%), Financials (-0.04%), and Industrials (-0.05%) followed suit with minor decreases.

Currency Market Updates

In recent market updates, the US dollar index showed a slight rebound after a 4% decline following the November 1st Federal Reserve meeting. This recovery was driven by short positions taking profits ahead of the release of the Federal Open Market Committee (FOMC) minutes. However, the dollar’s decline had been influenced by soft data on jobs, CPI, and retail sales, contributing to market volatility. Despite falling Treasury yields, profit-taking affected the Nasdaq index, reflecting the broader susceptibility of markets to traders’ profit-booking strategies. The dollar’s trajectory remains tied to economic forces, exemplified by existing home sales falling below forecasts and hitting their lowest since 2010, indicating the substantial impact of the Fed’s 5.25% rate hike, which could continue to exert pressure on the dollar’s value.

Meanwhile, in currency pairs, the EUR/USD saw a 0.33% decrease, retracting from earlier gains and hovering around the 61.8% Fibonacci level. The market sentiment differs between pairs, with USD/JPY showing increased speculative long positions compared to EUR/USD, potentially influencing a downward trend. Expectations regarding rate cuts diverge between the European Central Bank (ECB) and the Federal Reserve, with markets leaning towards rate adjustments in April for the ECB and May for the Fed. Additionally, the Sterling rose to a 10-week high against the dollar, backed by relatively hawkish comments from Bank of England speakers, despite market pricing predicting a potential rate cut by June. Other currency pairs, such as USD/CAD and USD/CNY, exhibited varied movements influenced by economic indicators and reports, underscoring the complex interplay of factors affecting currency markets. Looking ahead, upcoming releases like U.S. durable goods and jobless claims are anticipated to impact market sentiments and currency valuations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Corrects from Three-Month High Amid Dollar Strength

The EUR/USD pair retreated on Tuesday following a recent peak, marking a corrective move amidst a weaker US Dollar. Factors including steady yields and a dip in equities favored the Greenback, causing the Euro to lag. US data revealed a larger-than-expected drop in Existing Home Sales, impacting market sentiment. Meanwhile, upcoming reports like Jobless Claims, Durable Goods Orders, and the University of Michigan Consumer Sentiment will likely influence further market movements. The FOMC minutes reiterated concerns about inflation, signaling potential future tightening measures. The Euro’s performance was also affected by a decline against the GBP, with anticipation building for the Eurozone’s preliminary November PMIs as the next key report.

In technical analysis, the EUR/USD is showing a strong upward trend on early Tuesday just to end the day weaker able to reach the middle band of the Bollinger Bands. It’s currently trading just around this level, indicating the possibility of another upward movement. The Relative Strength Index (RSI) at 57 shows a neutral but slightly bullish stance.

Resistance: 1.0956, 1.1004

Support: 1.0885, 1.0832

XAU/USD (4 Hours)

XAU/USD Surges Towards Key Resistance Amidst Dollar Stability

Spot Gold demonstrated a robust surge on Tuesday, rallying from sub-$1,980 levels to approach a significant resistance mark at $2,010. This bullish movement occurred despite a dip in stock prices and a stabilized US Dollar. The climb coincided with steady US yields, showcasing resilience after briefly touching $2,007 before retracing toward $2,000. The prevailing upward bias hinges on the anticipation that the Federal Reserve has halted interest rate hikes, bolstering Gold’s appeal. However, while market attention focuses on the upcoming FOMC minutes and critical US data releases like Jobless Claims and Durable Goods Orders, a more aggressive Gold rally may hinge on a clear downturn in Treasury yields signaling a peak, as of now, keeping the metal’s surge subdued.

In technical terms, the analysis shows that XAU/USD moved higher on Tuesday, able to reach the upper band of the Bollinger Bands. The gold price is currently moving back below this band, suggesting a possible minor increase to reach back to the upper band. With the Relative Strength Index (RSI) at 63, it signals a continuing slight bullish trend for the XAU/USD pair.

Resistance: $2,008, $2,040

Support: $1,993, $1,973

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| USD | Unemployment Claims | 21:30 | 226K |

| USD | Revised UoM Consumer Sentiment | 23:00 | 61.1 |