Market Focus

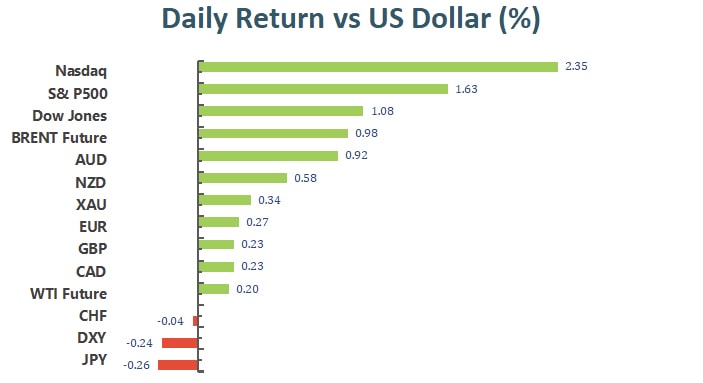

After the Federal Reserve announced that it will accelerate the reduction of monthly asset purchases in the context of rising inflation, three indices hit theirs best gain in a week on Wednesday. The Fed stated that it will increase its bond purchases by $30 billion per month in January, which is twice the $15 billion per month announced in November. The timetable for raising interest rates is advanced. It is expected that the interest rate will be raised up to three times next year, and then three more in 2023, bringing the Fed’s benchmark interest rate to 1.6%. The risk sentiment has improved after the statement was announced, because before the Fed meeting, the sentiment of monetary policy tightening was tense, and the previous increase has been basically digested. At the end of the market, the Dow Jones Industrial Average rose 1.1% to 35,927.44 points, the S&P 500 index rose 1.63% to 4,709.85 and the Nasdaq Composite Index added 2.1%.

In the S&P 500 sector, the only loser is the energy sector. The main reason is that people are still worried about oversupply, although people are still worried about Omicron’s threat to travel and energy demand, making energy still under pressure and oil prices still falling. Devon Energy, Occidental Petroleum and Diamondback Energy fell more than 2%. On the other hand, the biggest winner of the index sector is undoubtedly the technology sector related to interest rates. With interest rates unchanged, the technology sector led to a rocket up. Nvidia and AMD lead the technology sector, followed by Alphabet, Microsoft, Facebook and Apple, contributing to the index’s performance.

Main Pairs Movement:

Before the Fed’s monetary policy decision was released, market participants expected that monetary policy would be tightened and accompanied by nervousness. This caused the DXY to soar to almost annual highs, but then interest rates remained unchanged, and the only news is that they will speed up the reduction in bond purchases starting in January 2022, so the dollar index turned south and closed at 96.33.

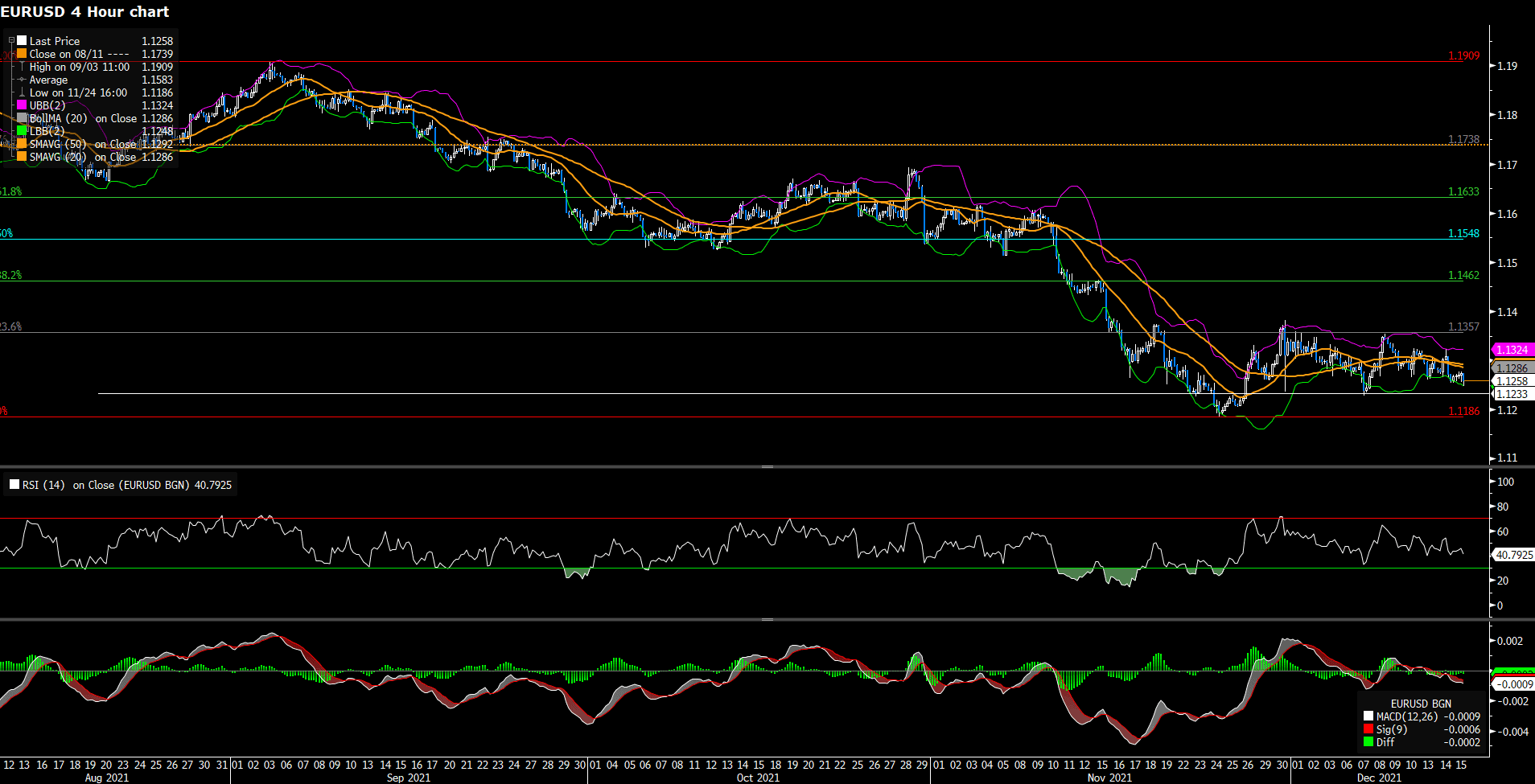

The EUR/USD is close to the 1.1300 level, but it was still below that level before the European Central Bank meeting, which will be held on Thursday. The ECB will announce its monetary policy decision, but the market is generally expected to maintain the current policy, this means the euro is hardly to get extra impetus.

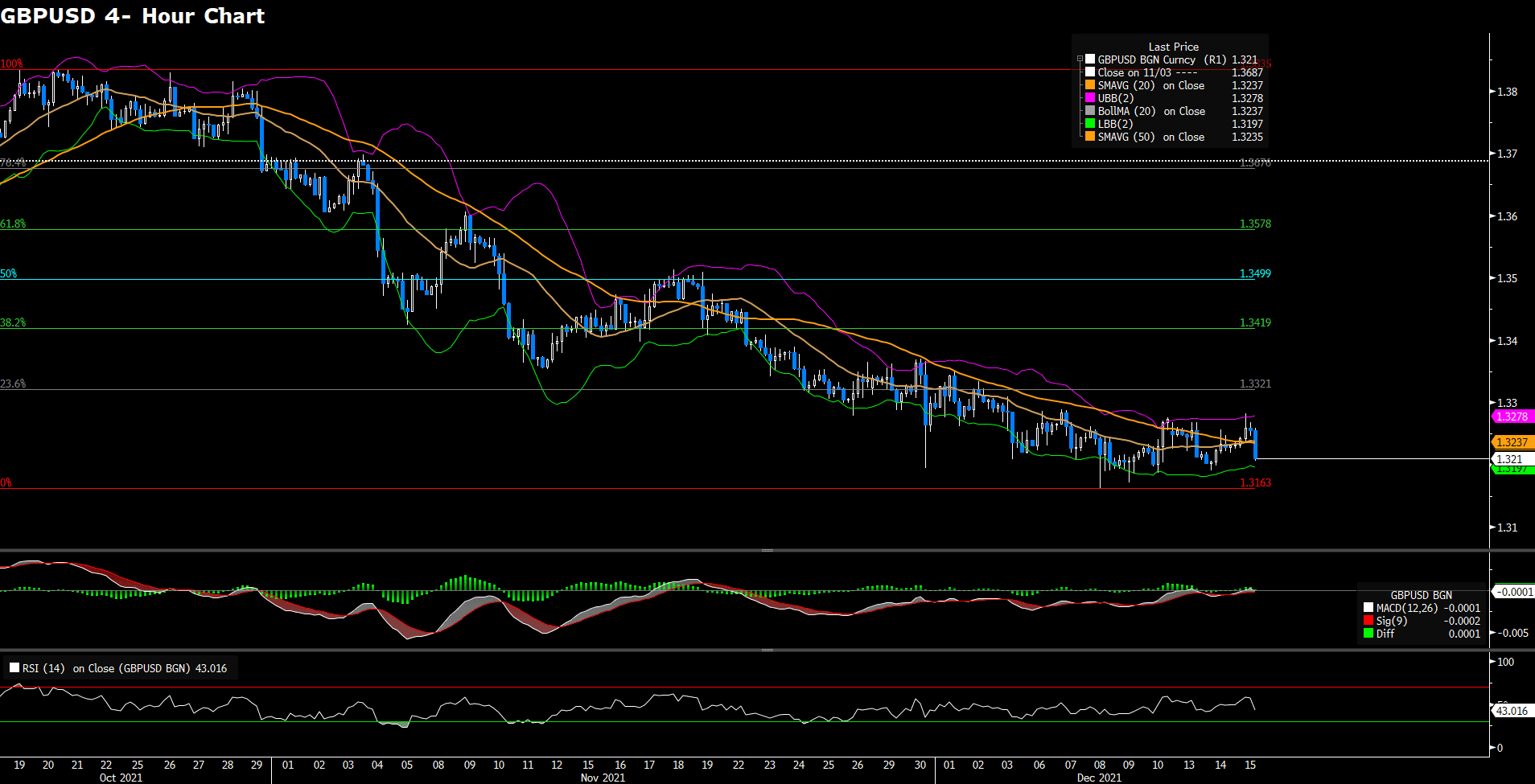

GBP/USD closed at 1.32582, also staying at recent levels without any breakthrough. The UK will announce its PMI later on Thursday, which may provide some strength for the pound.

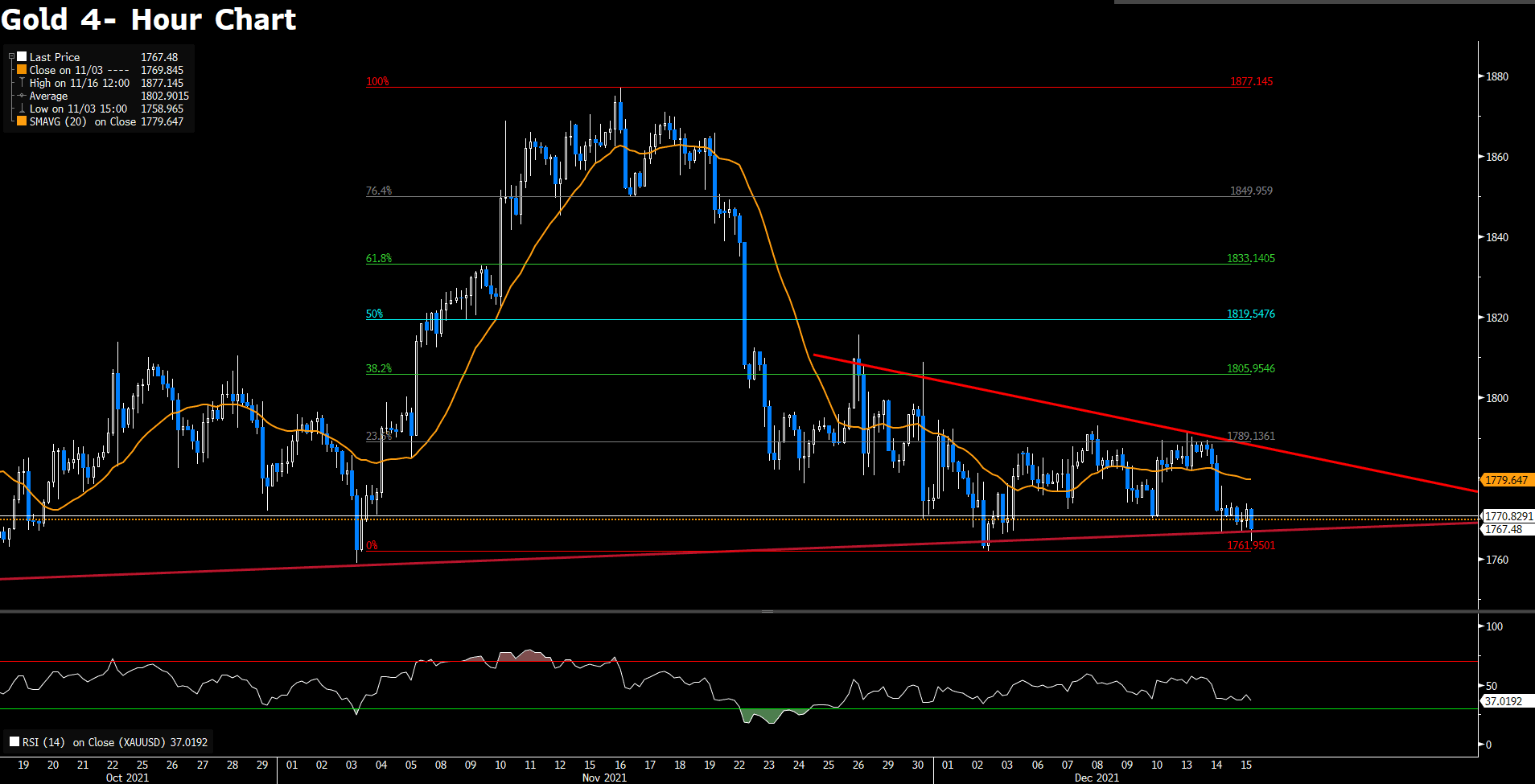

Gold hit a new low of 1,752 in several months and then rebounded to around $1,778 per ounce. Crude oil prices have risen with the stock market, and WTI is currently trading at approximately $71.50 per barrel.

Technical Analysis:

Gold price struggles to rebound, hovering below 1770, as focus shifts to FOMC meeting. Gold price is undermined since the market expects the hawkisk Fed will pace its tapering and the interest rates. From the technical analysis, as the time of writing, gold bears now target the descending wedge around 1765. Gold will re- confirm a bearish outlook if the wedge is breached downwardly. Alternatively, the recovery now needs to face stiff resistance at 1770, followed by 1789, in order to turn a bearish- to- bullish trend on the 4- hour chart. However, it looks like bears are still in control as the RSI indicator has not reached the oversold territory, suggesting a continuation of selling pressures. And the next relevant support is at 1761.

Resistance: 1770, 1789, 1805

Support: 1761

GBPUSD declined toward 1.3200 after the soaring UK inflation report, resulting in a renewal of the US dollar demand. From the technical perspective, the outlook of the currency pair becomes bearish on the 4- hour char as it trades below its 20 and 50 simple moving averages, indicating a bearish condition in the near- term. Since the RSI has not yet reached the oversold condition, sellers are still in control; thus, GBPUSD is expected to head toward its immediate support at 1.3163. Furthermore, the MACD is also turning negative as the time of writing, meaning that the pair has essentially turned from buying to selling. On the upside, GBPUSD’s bulls need to climb above the static level at 1.3321 to reclaim positive move. More price action will eye on today’s FOMC meeting and tomorrow’s ECB meeting.

Resistance: 1.3321, 1.3419, 1.3499

EURUSD declines merely trading at 1.1250 as the US dollar’s momentum picks up. From the technical aspect, EURUSD looks to test its immediate support at 1.1233, followed by 1.1186. The outlook remains neutral in the near- term as the technical indicator, RSI, lacks directional strength, steadily holding slightly below 50th mark. The support level at 1.1233 could be breached with the US Fed’s announcement later; if that is the case, EURUSD will become bearish in the near- term. On the upside, the currency pair needs to extend further north above the acceptance level at 1.1357 in order to turn upside.

Resistance: 1.1357, 1.1462, 1.1548

Support: 1.1233, 1.1186

Economic Data

|

Currency |

Data |

Time (GMT + 8) |

Forecast |

||||

|

USD |

FOMC Economic Projections |

03:00 |

N/A |

||||

|

USD |

FOMC Statement |

03:00 |

N/A |

||||

|

USD |

Fed Interest Rate Decision |

03:00 |

0.25% |

||||

|

USD |

FOMC Press Conference |

03:00 |

N/A |

||||

|

NZD |

GDP(Q3) YoY |

05:45 |

-4.5% |

||||

|

GBP |

Composite PMI |

17:30 |

57.6 |

||||

|

GBP |

Manufacturing PMI |

17:30 |

58.1 |

||||

|

GBP |

Services PMI |

17:30 |

58.5 |

||||

|

EUR |

ECB Monetary Policy Statement |

20:45 |

N/A |

||||

|

EUR |

ECB Interest Rate Decision (Dec) |

20:45 |

N/A |

|

USD |

Building Permits (Nov) |

21:30 |

1.663M |

|

|

USD |

Initial Jobless Claims |

21:30 |

200K |

|

|

USD |

Philadelphia Fed Manufacturing Index (Dec) |

21:30 |

30 |

|