As we approaching the last trading weeks of the year, upcoming week from Monday, Dec 16, to Friday, Dec 20, 2024, is loaded with important central bank policies and key economical data, presenting notable trading opportunities and risks at the same time.

KEY ECONOMIC INDICATORS

Central Bank updates:

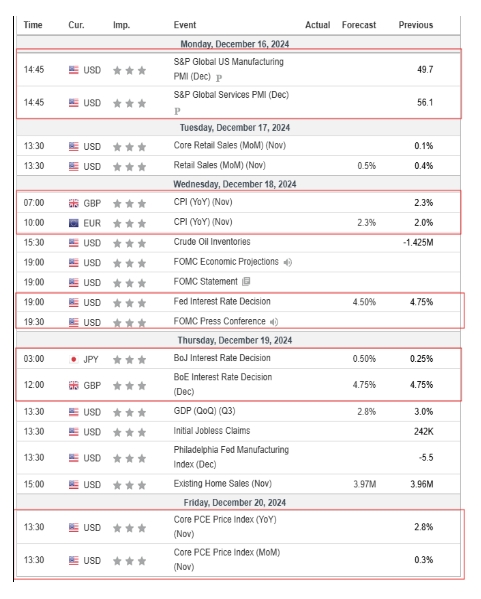

- Fed interest rate decision: The Federal Open Market Committee is most likely to cut interest rates again next week on December 18 to 4.25% to 4.5%, according to fixed-income markets and the tone of two recent speeches from Federal Reserve governors. Prediction site Kalshi currently gives a similar 73% chance of a cut. More economic data on jobs and inflation will come before the FOMC meets. However, a cut appears likely due to subdued inflation and a somewhat softening jobs market.

- BoJ interest rate decision: Latest news from Reuters Tokyo shows The Bank of Japan is leaning toward keeping interest rates steady next week as policymakers prefer to spend more time scrutinising overseas risks and clues on next year’s wage outlook. Any such decision will heighten the chance of an interest rate hike at the central bank’s subsequent meeting in January or March when there will be more information on the extent to which wage hikes will broaden next year.

- BoE interest rate decision: The rate will most likely remain unchanged for this month, as the market is pricing in that the Bank of England base rate will most likely be cut again in February 2025 to 4.5%.

Core PCE price index (November):

Core PCE, which strips out more volatile items like food and fuel, came in at 2.8% annually last month, with a 0.3% grow month-on-month, in line with expectations. This month’s core PCE data will directly impact Fed next move on the interest decisions.

MARKET MOVER

XAU/USD – (bullish outlook)

- While the expected downside move is corrective, it presents a strong risk/reward opportunity today.

- The strategy is to buy on dips.

- The primary trend remains bullish.

- Buying activity resumed at the 50% retracement level of 2663.7.

- Dip buying provides favourable risk/reward potential.

Trade Opportunity: Target 1: 2715.5 // Target 2: 2725.5 // Expires: 14 December 2024

GER40 DAX – (bullish outlook)

- The overall trend remains bullish.

- Price action is consolidating near all-time highs.

- The 20474 level has proven pivotal.

- A breakout above the recent high at 20474 is likely to trigger further upside.

- We anticipate gains to continue extending today.

Trade Opportunity: Target 1: 20831 // Target 2: 20931 // Expires: 14 December 2024

EUR/USD – (bearish outlook)

- Selling pressure from 1.0531 erased all initial daily gains.

- The pair has posted five consecutive daily losses.

- Rallies remain capped as sellers dominate.

- Key support is identified at 1.0420.

- The preferred strategy is to sell on rallies.

Trade Opportunity: Target 1: 1.042 // Target 2: 1.04 // Expires: 14 December 2024

MARKET NEWS

Foreign Exchange:

- The U.S. Dollar Index advanced by 0.28 points, reaching 106.99, reflecting continued strength in the dollar amid shifting monetary policy dynamics globally.

- EUR/USD slid by 28 pips to 1.0466, marking its fifth consecutive daily decline. The pair faced additional pressure after the European Central Bank (ECB) followed through on expectations by cutting its key interest rates by 25 basis points, signalling a more dovish stance in response to slowing economic growth across the eurozone.

- USD/JPY edged higher, gaining 19 pips to settle at 152.64. The yen continued to weaken as markets speculated on the Bank of Japan maintaining its ultra-loose monetary policy, in stark contrast to the Federal Reserve’s hawkish tone.

- GBP/USD tumbled by 81 pips to 1.2669, reflecting broad dollar strength and lingering concerns about the UK’s economic resilience amid tightening financial conditions.

- USD/CHF surged by 79 pips to 0.8921 after the Swiss National Bank (SNB) surprised markets with a 50-basis-point rate cut, bringing its key rate down to 0.50%. This move exceeded the widely anticipated 25-basis-point reduction, intensifying downward pressure on the Swiss franc.

- AUD/USD saw a modest dip of 3 pips, closing at 0.6365. The pair remained range-bound as traders weighed weaker domestic data against a stable dollar.

- USD/CAD climbed significantly, rising by 61 pips to 1.4218. The Canadian dollar weakened amid a combination of falling oil prices and robust U.S. economic data, which further bolstered the greenback’s dominance.

Commodities and Stocks

- On Thursday, U.S. markets extended their losses, with the Dow Jones falling 234 points (-0.53%) to 43,914, the S&P 500 dropping 32 points (-0.54%) to 6,051, and the Nasdaq 100 down 148 points (-0.68%) to 21,615.

- Warner Bros. Discovery surged 15.43%, leading the S&P 500 after announcing a restructuring of its streaming and networks businesses.

- The 10-year Treasury yield rose 5 basis points to 4.324%, while U.S. producer prices grew 3.0% in November, exceeding expectations. Initial jobless claims climbed to 242,000.

- European markets were mixed: the DAX 40 added 0.13%, the FTSE 100 rose 0.12%, and the CAC 40 dipped 0.03%.

- U.S. economic data showed producer prices rising 3.0% year-over-year in November, exceeding the expected 2.6%. Meanwhile, initial jobless claims climbed to 242,000, higher than the forecasted 225,000.

- In commodities, WTI crude slipped $0.27 to $70.02, ending a three-day rally.

Asian Session Updates

- During the Asian trading session, USD/JPY extended its upward momentum, reaching a high of 152.90. The move was supported by positive economic data from Japan, as the Bank of Japan (BoJ) released its latest Tankan survey.

- The Tankan large manufacturers’ business confidence index improved to +14 in December, up from +13 in September, marking the highest reading since March 2022. This uptick reflects growing optimism among Japanese manufacturers despite persistent global uncertainties.

- However, the yen’s continued weakness highlights the divergence between the BoJ’s dovish monetary policy stance and the Federal Reserve’s hawkish outlook.

- Elsewhere, major European currencies remained lacklustre. EUR/USD traded flat at 1.0465, with the euro showing little reaction to economic developments as traders digested the European Central Bank’s recent rate cut. Similarly, GBP/USD hovered near 1.2670, reflecting subdued market activity amid a lack of fresh catalysts from the UK.

Click here to open account and start trading.